Date: April 25th 2025

Time: 9:15am

The Homebuilding Situation stands at 18.17. This is 81 points below the Average Situation for Homebuilders. The situation improved by 6 points from the prior month.

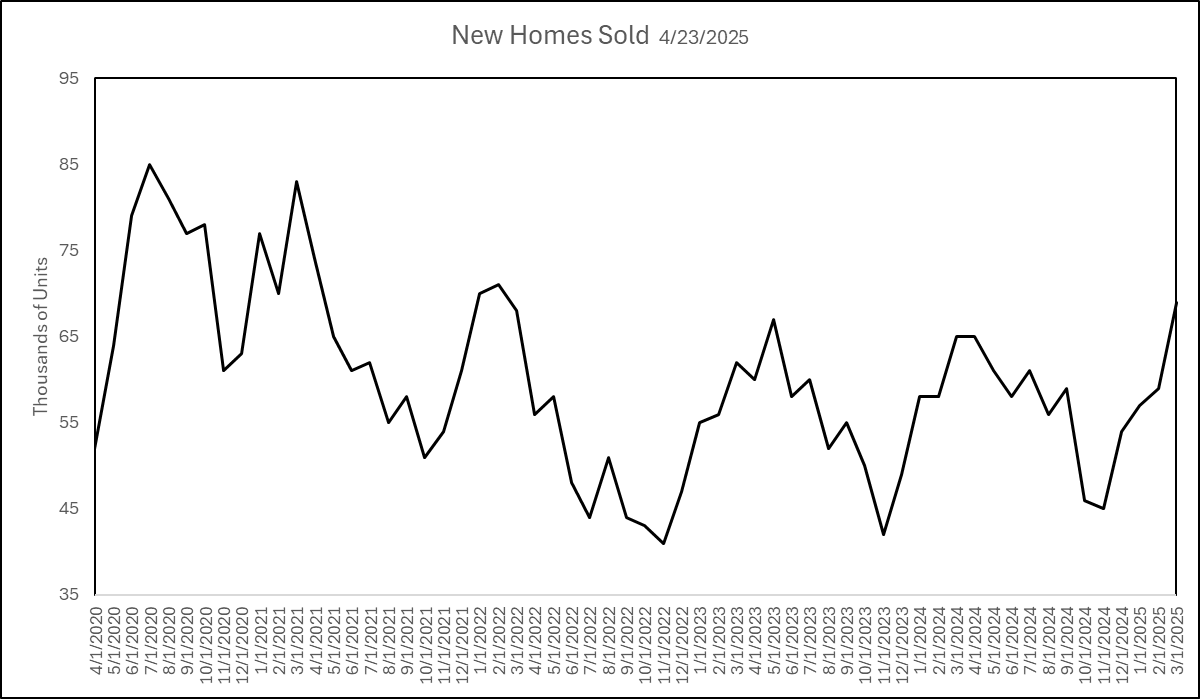

Sales

March saw a 3 year high of 69,000 units sold. This is the most sales since February 2022.

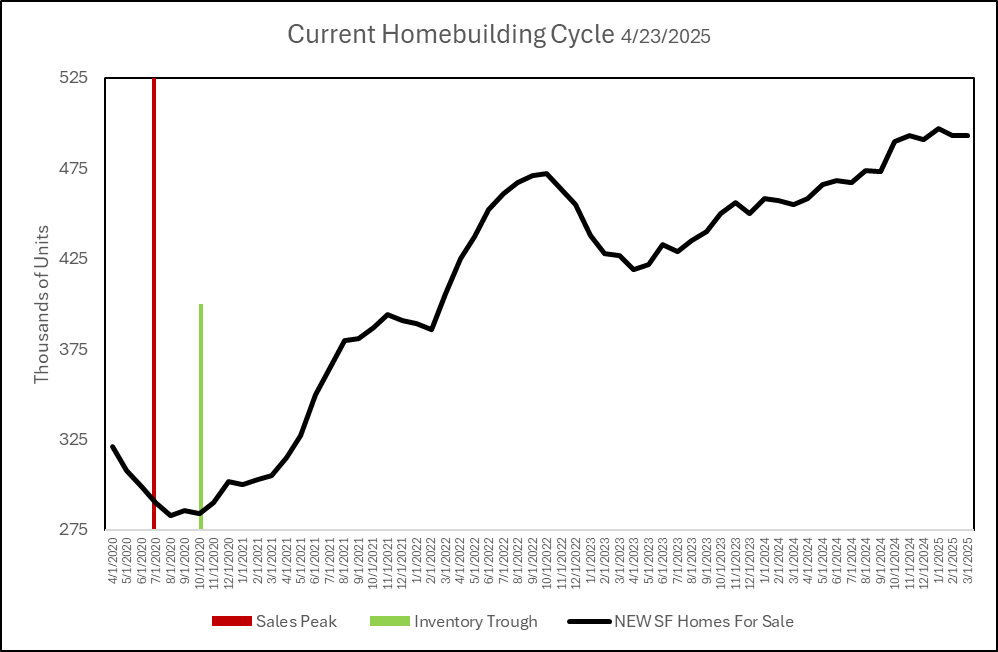

Inventory

Current new single family homes for sale remained at 493,000 units. Down 1k monthly. The past 6 months have been revised to remain under 500,000 units on a non seasonally adjusted basis. In February, the seasonally adjusted rate remained above 500,000 units, at 503,000. The most since November 2007 which saw 508,000 units for sale.

Price Direction

Price decreased year over year by -7.5%. The Median Sale Price for a New Home was $403,600. The past 4 months received revisions to pricing.

Mortgage Rates

Mortgage rate decreased by 2.5% month over month. March’s average 30yr Fixed Mortgage Rate was 6.65%

Additional Commentary:

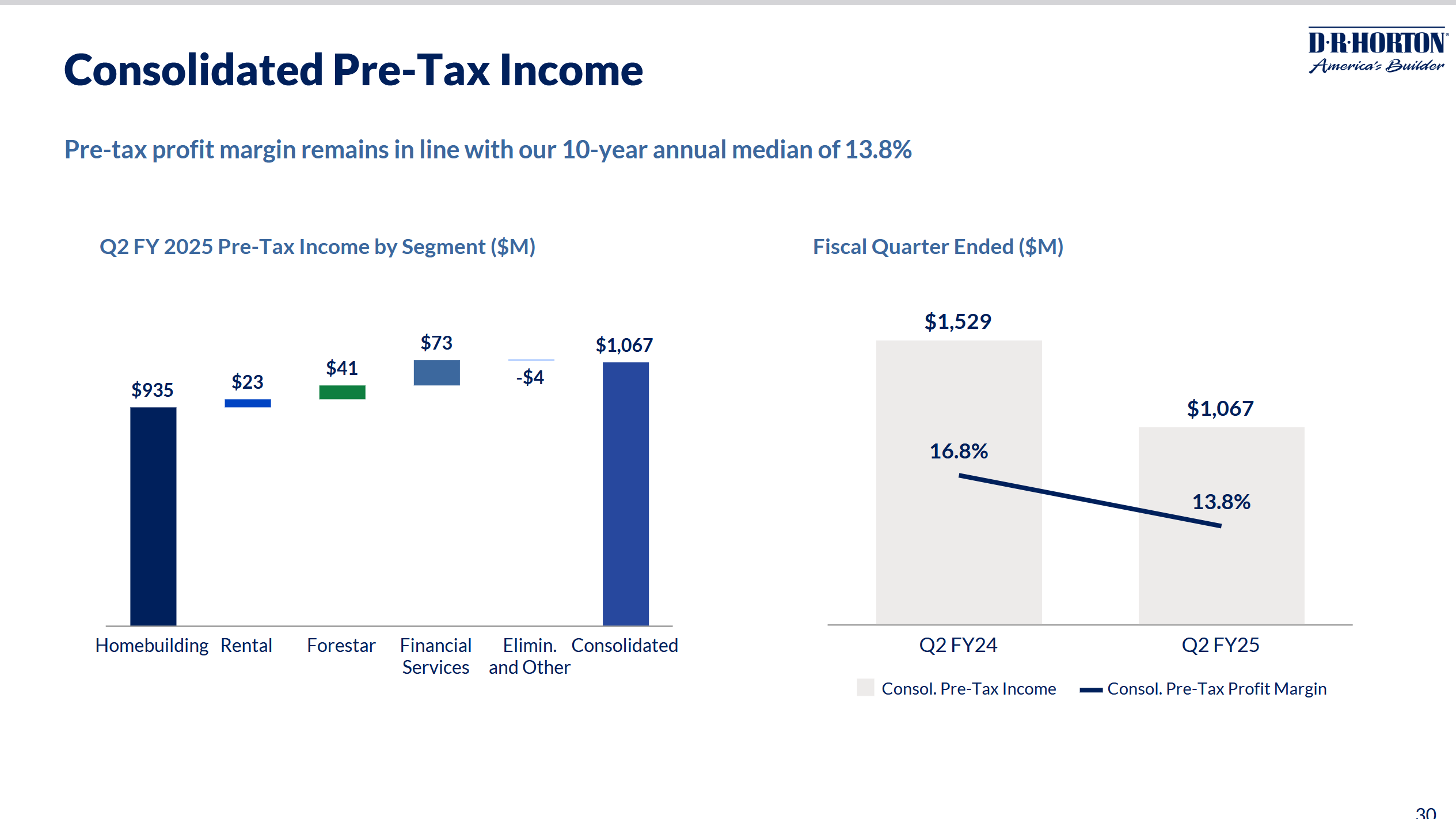

Public builders posting quarterly results have left the margin compression conversation and entered the reduced income conversation. Leading the way, DR Horton, the Nation’s largest builder not only saw sales declines, but pre tax profits were cut by over 30%. Chart below.

Beazer Homes saw drastic reductions in Net Income. The chart below will speak for itself.

Taylor Morrision saw net sales decrease 8% while Pulte saw 7% decrease. Pulte joined DR Horton with a 22% decline in Net Income year over year. Pulte had been fairing better than most until recently.

The carnage in Homebuilder stocks has slowed pace, albeit the drop has been precipitous thus far, with #2 builder Lennar seeing a 52 week low in share price equating to a 48% loss in share value. If the trend continues of decreased Net Income, the share value and market cap on the publicly traded builders will likely fall even further.

Each builder reporting has made light of “constrained affordability” for buyers. Until and if the price of money comes down, expect the actual price of product to be in the crosshairs to keep pace moving forward. Especially if the -7.5% YOY price change along with incentives moved sales pace to new highs. This may signal the start of a “race to the bottom” in pricing, to grab market share and maintain declining revenues.

Vendors and Subcontractors should expect to see requests to share in the cost reduction efforts across the board.

Builders with product in the sub $370,000 range will likely be per community count sales leaders, and Smaller builders with product mix targeting entry home pricing in their markets should begin to see opportunity to compete with the larger builders in their markets as operating cost pressures mount for their larger peers.

The more inventory moves, the more the Homebuilding Situation will improve, even if it means the balance sheet situation for big builders worsens.

The Method and Research for the index is available Here:

https://www.uspropertyservices.com/homebuilding-situation-index

DR Horton Income

Beazer Homes Income

Pulte Homes Income

Lennar Share price. See 52 Week Range.