Real Estate Roundup

The Good, The Bad and The Ugly

The Memo:

To:

Everyone

Re:

8 bullet points of recent news on the real estate industry at large.

Inter Department Directives

From:

Mr. Awsumb

The Good

Texas Stock Exchange files with S.E.C. to operate as a National Exchange, targets 2026 launch and listings date.

This gives another avenue for Builders and Developers (obviously amongst others) to access equity capital. I wouldn’t be surprised to see a few solid Texas outfits go public here if and when the exchange begins operations, as sign posts.

Boxabl gets approved in California as a modular home builder. (See wildfire relief efforts)

TreppWire is reporting Private Label CMBS issuance is on the rise. CMBS issuance outpaced Whole Loan origination in 2024.

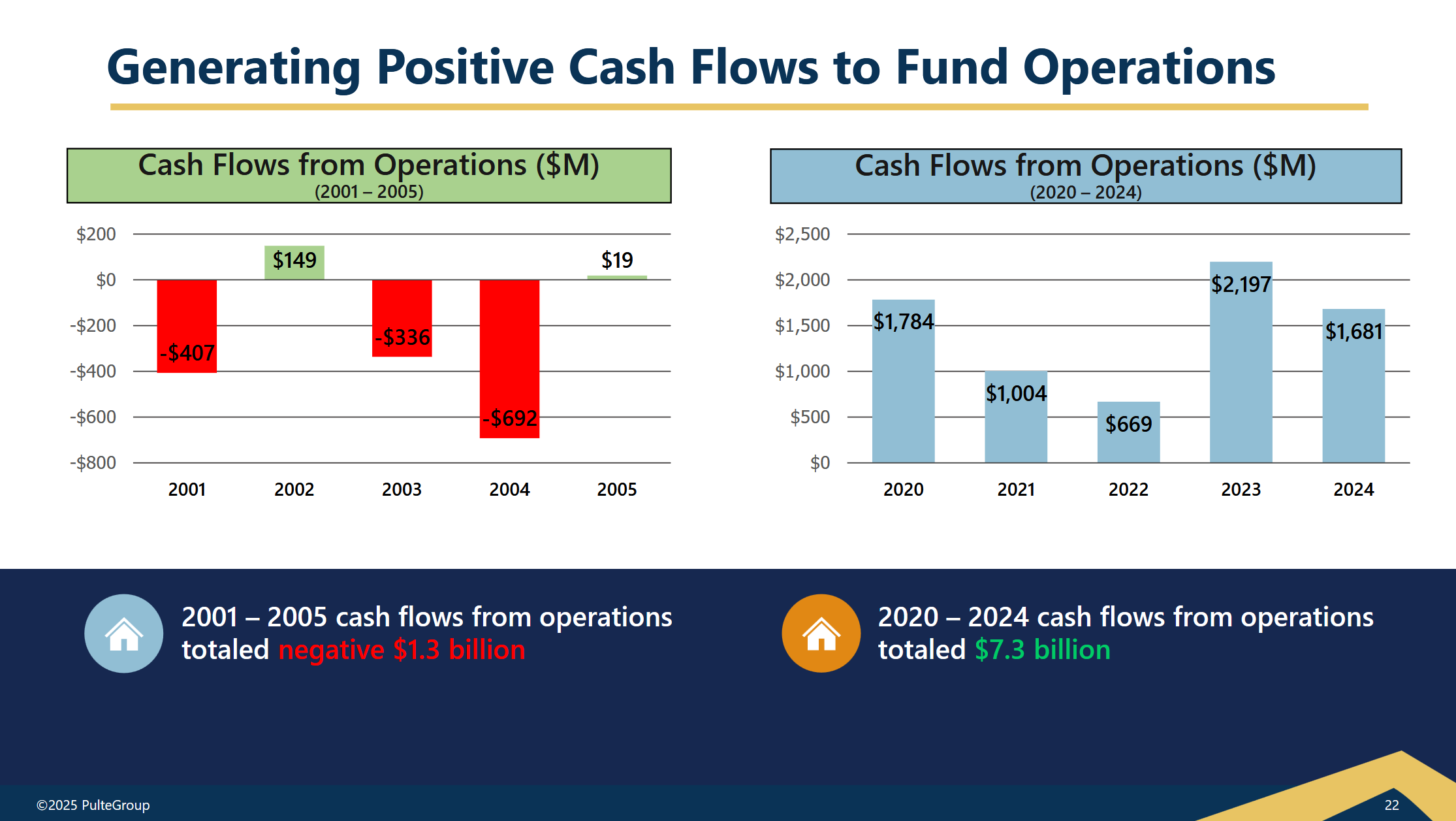

Pulte Homes reported Q4 earnings. They're performing incredibly well considering the circumstances the entire industry faces. Give credit where it's due.

The Bad

1031 Exchange Deal Volume hits 12 year low.

The National Association of Homebuilders sent a letter to The President asking to exempt building materials from Tariffs on Canada and Mexico (see attachment). They were not exempted. Lumber futures closed Friday at $592 per 1,000lb ft. Friday’s trade volume was also up considerably. Add 25% and watch permits from here.

Pulte Homes is the 3rd largest homebuilder in the country. They've now joined DR Horton (#1 in sales volume) in calling out the similarities to the market change in 06/07 in their investor presentations for earnings calls, as a way to show they are better capitalized. Share buybacks however are still on the menu for now.

The Ugly

US Logistics Rents fall for first time in 15 years.

Rents down 7% year over year.

Vacancy increased again. Up to 7.1% in Q4 of 2024.

There's still plenty more new industrial supply coming to market.

Inter Department Directives:

Topic: Risk Mitigation

CoStar is reporting private label short term floating rate lending has already surpassed all of Q1 2024 levels. They note new offerings tied to SOFR + spread (Single Overnight Financing Rate)

For our Real Estate Dept.:

A reminder that SOFR is based on the underlying value of collateral for overnight borrowing cash. Namely treasuries. It's also volume weighed. So while SOFR appears to be lowering, there's ample notes, bills and bonds out there with values above the current rate now. And SOFR has seen sudden spikes, to the point they've even spooked the Fed. For the near term outlook, using the SOFR index for the trend of SOFR (up) may be a prudent risk mitigation tool when assessing short term financing needs for our real estate portfolio. Run a report on that asap. Let's not get stuck wiping out cash flow over one month of elevated rates because a regional bank decided to pledge all their higher yield treasuries as collateral all at once or because of quarterly tax bills.

For our Finance Dept.:

Please have a plan in place to assess risk of DSCR (debt service coverage ratio) factors, and a plan for extension or modification in the event SOFR + Spread (or overly optimistic calculations) puts the RE Dept. into NP (non performing for everyone else) territory. Also lets run a report on how long the extension can be before the situation becomes onerous.

For our Purchasing Dept.:

There’s 2,467 sawmills in the US. Start making calls. Also, Thomas is a great resource for finding US Manufacturers, they even have a handy supplier discovery search feature on their site.

Team: Remember, hope isn't a solution. But there's no solution without hope that there is one, or hope that it works.

“We're in the business of doing business, so let's get back to business.”

-Monty Brewster, Brewster’s Millions

Sincerely,

Please CC your colleagues. I’m sure I forgot to copy someone.

None of this is financial or investment advice.

End memo.

Attachments:

The letter from NAHB

SOFR

SOFR Index

Pulte Comparison

DR Horton Comparison