Friday Effing Memo

Spring. Or something like it

The Memo:

To:

The Team

Re:

The next 5 weeks.

Comments:

We just completed week 159 of the current rate cycle. By nearly all accounts, human behavior seems to be repeating itself. Again.

After another down day in the markets, we are quickly approaching historical inflection points at week 163. We will likely see a bounce before May in the 4 indices outlined above. 1 of the past 3 cycles continued higher for longer, only to end in the same fashion. The extended cycles bear the same patterns.

Entering April economic conditions include:

New Tariffs?

Mortgage rejection rates at 40%+

30 year avg. mortgage rates at 6.8%

Homebuilder margins compressing

Gold skyrocketing.

By May, there May well be less uncertainty about the situation.

End Memo.

The Report

Within the next 4 weeks, currency directions will likely prove more clear.

I have no idea what stops this train.

You may read headlines about gas/oil increasing for summer season. I say it’s clockwork.

If you read headlines about unseasonally high layoffs or claims in early May, you expected it here. April may be muted.

It’ll likely fade as people seem to never remember that:

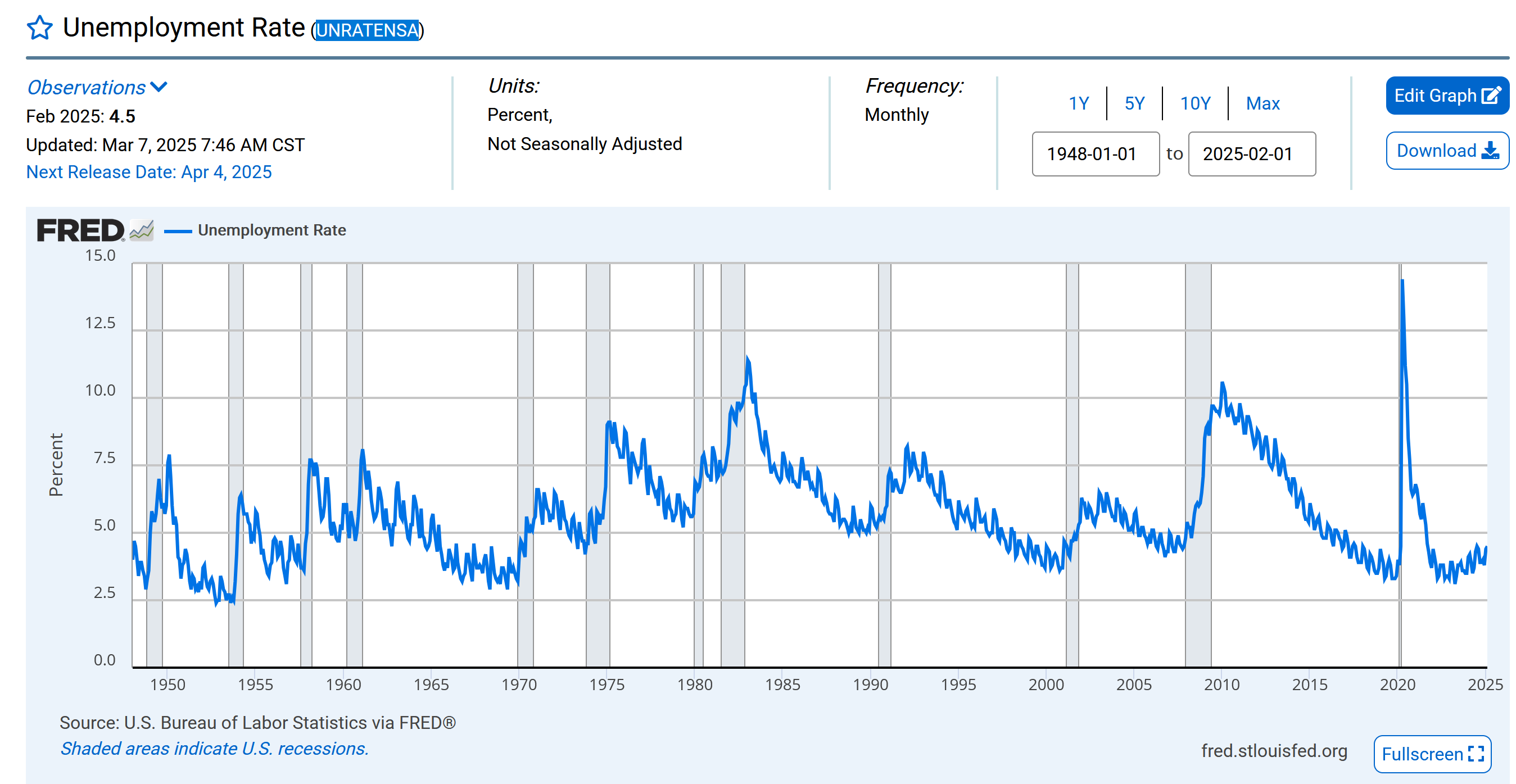

Initial Claims peak at the end of/after recession.

Continuing claims peak after recession

Unemployment peaks after recession.

Becuase job losses are a byproduct of receding business activity. Expanding margins don’t need to trim headcount. But compressing margins do.

Also, a note on construction employment strength, as we have some public builders now addressing said margin compressions:

Not only did the US just have the most amount of housing under construction in recorded history, but until January 2024, we had the most amount of housing units under construction per construction employee in history as well (outside 2 months in 2020).

We’re back to 1986 Levels, and still well above pre GFC.

See you next Friday.